Getting started with machine learning models can seem to be an overwhelming task if data is incomplete, the return of investment expected instantly and business ethics left undiscussed. Early experiments and a long term strategy, however, can help establish a competitive edge and help decision makers transform data into business critical solutions.

In this article, you will learn:

- Why long term success with machine learning requires early and focussed experimentation that fails fast.

- How new technologies provide better data for decision making.

- The essentials of machine learning and how it differs from current insurance calculation models.

- How to get started and reap the hidden value in your data.

Here is an example to illustrate my point:

According to a report from Teradata, 80 % of enterprises that are invested in machine learning or various branches of AI do it to enhance customer experience, minimise costs or manage risks. For insurance companies, two basic drivers contribute to the adoption of new technology:

Implementing new technology is only the first step in reaping the full benefits of digital. Often, applying machine learning methodologies is accompanied by an increase in costs, an apparent lack of results and plenty of frustrations. Setting the right expectations from the beginning is pivotal for later success.

Long term success requires early machine learning experimentation

More often than not, adopting machine learning will not yield instant returns. In fact, early machine learning implementation is associated with an increase in costs and requires a long term strategy to turn those into profit. This is due to the requirements of data quality and the explorative nature of the technology.

“According to a BCG analysis, more than half of the companies that invest in machine learning see no return to investment.”

– Tobias Lund-Eskerod, Delivery Director, Monstarlab

“If data isn’t representative, your models will be off. In the early stages, you’ll often find yourself with incomplete datasets, which either needs to become complete or the problem you are trying to solve needs to change” says Tobias Lund-Eskerod, Delivery director at Monstarlab, and continues:

“When applying the technology, unanticipated findings will very likely appear. These findings can have a big impact on the allocated budget for the project making it difficult to convince everyone about its potential”. But addressing the financial cost of machine learning seems to be just as important as the potential profit when asking IT decision-makers. According to Teradata, companies that have adopted machine learning technology are expecting a significant ROI in the future:

Expected ROI for every dollar invested in AI technologies

With executives aspecting ROI to triple in 10 years, the need for a long term strategy with continuous investments, multiple tests and evaluations is crucial. Yet, business leaders have a hard time committing fully to the technology due to the successful business model in insurance with high margins and stability for decades. Demystifying ML is critical for greater and earlier adoption.

Strengthening decision-makers by revealing new information

Training predictive models to process manual tasks and find patterns in structured, semi-structured and unstructured datasets to drive better business decisions are titillating for all insurance companies. But the reality is that even though they have tons of customer data, some are wary of the potential outcome when applying machine learning technology.

“The very core of an insurance company is to assess risks based on personal information and create matching policies. And because we’re all individuals, machine learning holds the potential of treating all of us differently from each other, which opens up for discrimination”, says Tobias Lund-Eskerod.

A vital part of every Insurance company is to break their entire customer base into smaller groups. But machine learning holds the potential of breaking groups down to a group of very few and assessing individuals based on inappropriate criteria such as race, gender, sexual orientation etc.

But even with this integral risk of machine learning, the technology is still based on data and mathematical methodologies, says Tobias Lund-Eskerod. Data that insurers select, clean and prepare as well as mathematical methodologies such as regression, classification and clustering. How insurers decide to interpret the outcome is entirely up to the business leaders. The technology in itself does not hold the power to discriminate, pose questions or solve problems. It does, however, have the potential to minimise costs, increase profits and, in particular, perform a more precise Customer Life Value calculation with minimal human intervention and guidance.

Applying machine learning to improve Customer Life Value – Example

Machine learning is only as good as the data presented. But with insurance companies only processing 10-15 % of their customer information, according to an Accenture survey, insurers are failing to utilise their insights to calculate precise CLV’s for their customers. Insights that could bolster valuable policies for both insurer and insured.

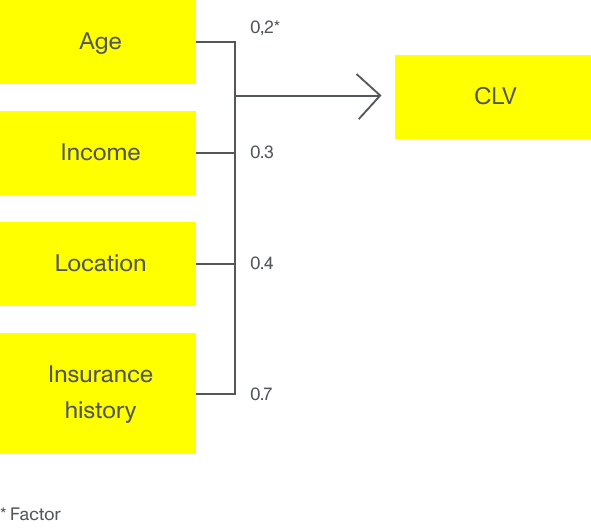

A common praxis for insurers is to use age, residence, external sociodemographic parameters as input for pricing and CLV determination. These parameters are often used in a GLM or multiple linear regression model where every input is given a factor, which has an impact on the CLV. For instance, a young customer in a quiet neighbourhood equals a higher expected CLV than a young customer in a neighbourhood statistically prone to thefts.

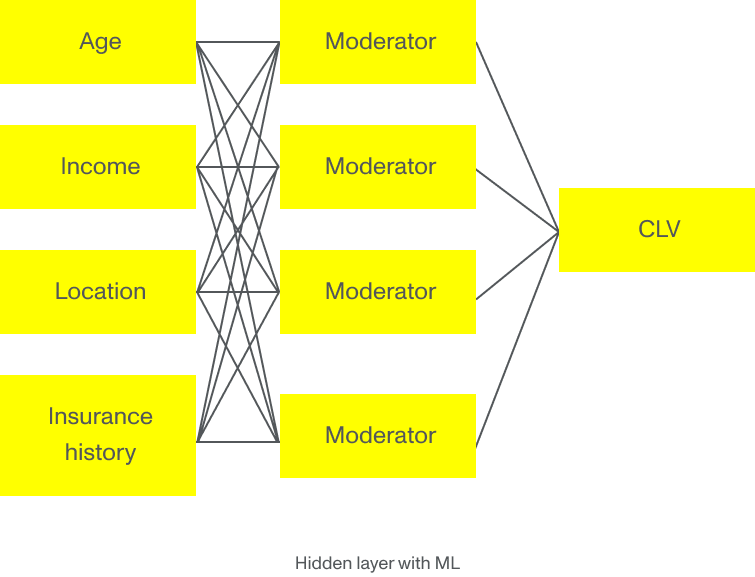

But imagine if the correlation was different. Imagine if the young customer living in the neighbourhood statistically prone to thefts is not as likely to fill out an insurance claim as the multiple linear regression model indicates. If we apply machine learning algorithms to this example, we feed the algorithm with tons of historical data about customers aggregated over time by the insurance company, statistical databases and government organisations. Presented with all of this data, machine learning models can identify underlying patterns and discover those parameters that really matter for calculating a more precise CLV. The single most important parameter for the young customer in the troubled neighbourhood might not be the location but rather education, marital status or numbers of insurance policies – or even all of them combined.

The complexity and sheer amount of information presented is simply too much for multiple regression models to cover. This is where new technologies such as machine learning and deep learning shows its proper weight by creating a more accurate valuation and prediction of the customers.

How to get started with machine learning

Even though insurance companies have experienced profitable margins and a sustainable business model for many decades, a majority of business executives do believe they must incorporate new technologies to remain relevant for their customers.

A common praxis for insurers is to use age, residence, external sociodemographic parameters as input for pricing and CLV determination. These parameters are often used in a GLM or multiple linear regression model where every input is given a factor, which has an impact on the CLV. For instance, a young customer in a quiet neighbourhood equals a higher expected CLV than a young customer in a neighbourhood statistically prone to thefts.

“According to a 2018 study, 82 % of business executives in the insurance sector believe they must be innovative in order to maintain a competitive edge. Yet, 77 % of them add that technology is advancing faster than what their company can adapt to”, says Tobias Lund-Eskerod.

In other words, getting familiar with machine learning now is important to stay relevant in the ever-changing landscape of digital. But getting started can feel like looking for a needle in a haystack. To get the wheels turning, decision-makers in insurance companies should start the machine learning journey by answering these three questions: